In our work across the GCC market, the most consequential question senior leaders bring to us has shifted from whether AI matters to what AI does to the consulting industry that helps deploy it. Boston Consulting Group's April 2026 disclosure that 25% of its $14.4 billion 2025 revenue came from AI work, roughly $3.6 billion, made the answer visible. The industry is splitting along two breakpoints: AI use, which is becoming table stakes, and rebuilt economics, which determines who survives the redistribution that follows.

This outlook examines seven shifts that define the bifurcation, from how AI revenue has become the firm-defining metric, through the productivity paradox forcing pricing reform, the trust failures that turn governance into a contractual term, and the squeeze on the mid-tier, to the orchestration model emerging as the practical answer. It closes on the GCC-specific variant where data sovereignty, localisation rules, and the Year of AI rewrite the structural rules for global firms and regional players alike. Each shift carries specific implications for buyers, providers, and the investors and new entrants now examining the GCC market.

This analysis draws on industry surveys, public firm disclosures, peer-reviewed research, market sizing data, regulatory and policy developments, and analyst and news coverage from late 2024 through early 2026. Sources include the IBM Institute for Business Value (n=400 C-suite, October 2024), BCG's AI Radar 2026 (n=2,400 executives), McKinsey & Company, KPMG, the Management Consultancies Association, Mordor Intelligence, the Hawaii International Conference on System Sciences (HICSS, 2025), and reporting in Bloomberg and Business Insider.

How has AI become the metric by which consulting firms are now measured?

AI has become the metric by which consulting firms are now measured. Public AI revenue disclosure is not new. Accenture has reported generative AI bookings quarterly since late 2023; IBM has reported AI revenue as a financial line for over a decade. What is new is that AI is now the lens for evaluating firm performance, and the largest single destination for consulting investment.

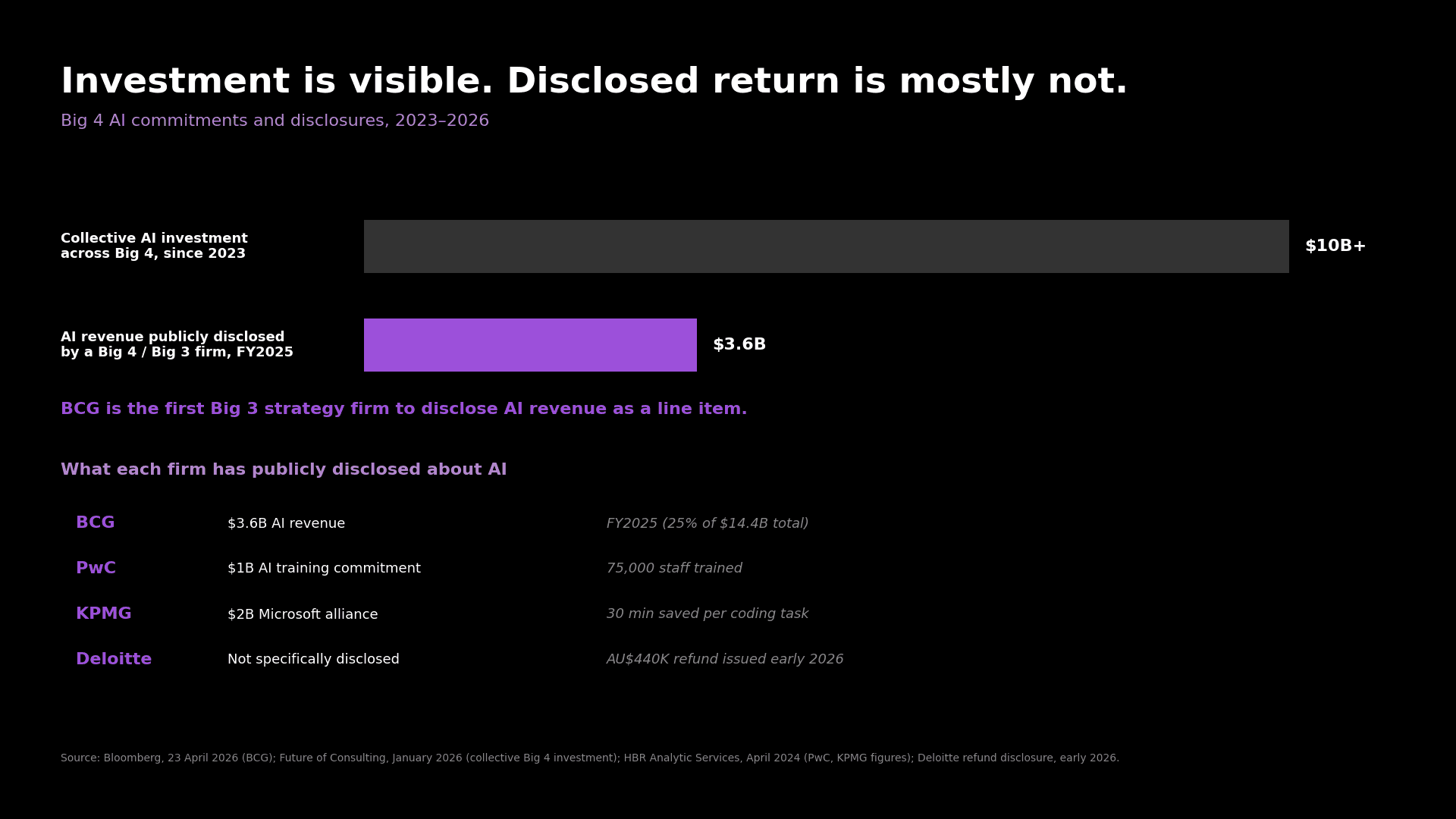

Boston Consulting Group's disclosure that 25% of its $14.4 billion 2025 revenue, roughly $3.6 billion, came from AI work (Bloomberg, 23 April 2026) is significant not because it was first, but because it was the first such disclosure from a Big 3 strategy firm. AI revenue had been a financial line for tech-services firms for years; inside MBB strategy consulting it had been hidden in broader "tech and digital" categories. The number made the position visible. CEO Christoph Schweizer called AI "value accretive" and embedded in the firm's highest-value functions.

Exhibit 1. Big 4 collective AI investment has passed $10 billion since 2023; only BCG has publicly disclosed AI revenue at scale ($3.6 billion / 25% of FY2025).

The capital allocation shift is the larger story. Big 4 collective AI investment has passed $10 billion since 2023 (Future of Consulting, January 2026). PwC's $1 billion commitment trained 75,000 staff. KPMG's $2 billion Microsoft alliance produces productivity figures of 30 minutes saved per coding task and 90 minutes per competitive intelligence study (HBR Analytic Services, April 2024). McKinsey senior partner Michael Birshan told the UK House of Commons in November 2025 that 25% of fees globally were linked to outcomes (Business Insider). BCG's headcount of 33,500 is now hiring AI engineers, IT architects, and data scientists in preference to traditional consultants.

For buyers, a firm with $1 billion of training spend and no disclosed return is not the same evidentiary basis as a firm with a measured number; the AI revenue benchmark is becoming a procurement question. For providers, boards, analysts, talent, and clients now read consulting firms through the AI lens, and firms without a defensible position will be measured by what they cannot show.

The consulting market is growing, but the redistribution is sharper than the headline

The consulting market is growing, but the growth is concentrating into fewer firms. Buyers expect to spend more on consulting overall, while consolidating their vendor lists toward firms they trust to deliver AI well. The redistribution is sharper than the topline number suggests.

The growth side. Corporate AI spend is forecast to double from 0.8% to 1.7% of revenue in 2026 (BCG AI Radar 2026, n=2,400 executives). The global AI consulting market is forecast at $14 billion in 2026, a 26.5% CAGR. UK consulting is forecast to grow 5.7% in 2026 and 7.4% in 2027 (Management Consultancies Association, January 2026). The signal had been visible earlier: the IBM Institute for Business Value's October 2024 survey of 400 C-suite executives projected consulting spend rising from 2.8% to over 4% of client revenue, an incremental $500 billion per year across the Fortune 500, with 86% of buyers expecting to spend more.

The consolidation side. The same IBM survey found 70% of buyers will buy from fewer, more trusted organisations because of AI. The growth pie expands; the share going to trusted firms expands faster. Buyers are not adding new providers; they are concentrating spend with the few they trust to deliver AI well.

The structural reason. AI does not displace the consultant; it amplifies the consultant who can use it. Peer-reviewed analysis of consulting practitioners published in 2025 reaches the same conclusion as buyers: AI augmentation, not consultant displacement, is the dominant operating pattern (HICSS, 2025). The growth in AI consulting is a redirection toward consultants who can deliver with AI, not away from consulting itself. Firms that demonstrate this capability capture disproportionately. Firms that cannot are crowded out, even in a growing market.

For buyers, the question is no longer "should we spend more on consulting?" but "with whom?" Trust criteria, governance, and demonstrated AI delivery now matter more than firm scale. For providers, top-tier capture intensifies and mid-tier capture narrows. For investors and new market entrants, a market that is both growing and consolidating rewards entry by firms with a defensible position on AI delivery.

The productivity paradox is forcing pricing reform that lags the technology

Pricing reform lags the technology. AI has materially compressed consultant task time on routine analytical work, but most consulting revenue is still time-billed. The gap between AI productivity and time-based revenue is structural, not transitional, and the pace of pricing reform is the binding constraint on which firms come through the bifurcation intact.

The pricing transition is real but partial. McKinsey senior partner Michael Birshan disclosed in November 2025 that 25% of fees globally are linked to outcomes (Business Insider, November 2025). EY has publicly discussed a service-as-software pricing model. 67% of consulting buyers now prefer fixed-fee engagements over time-and-materials, up from 41% three years ago (Deloitte, 2025). 73% want new pricing models because of AI (IBM IBV, October 2024). Three quarters of McKinsey fees, however, remain on traditional billing. The direction is set; the pace lags.

The productivity gain that drives this pressure is real and measured. KPMG's internal data shows generative AI saves 30 minutes per coding task and 90 minutes per competitive intelligence study (HBR Analytic Services, April 2024). Earlier Harvard Business School and BCG analysis found consultants using AI completed tasks 25.1% faster with 40% higher quality. Two and a half years on, productivity has compounded with maturing tooling; pricing has not moved in proportion.

The structural reason is that pyramid economics depend on junior staffing. Big 4 AI investment over the past three years has been directed at tooling, not at rebuilding the compensation and pricing structures that determine margins. The work most vulnerable to AI is the same work that funds entry-level consultant training: research, analysis, documentation, first-draft deliverables. As that work is automated, the apprenticeship pipeline narrows. Senior-led delivery the next decade requires has fewer people training into it. MIT 2025 research reinforces the pattern: 95% of generative AI projects deliver zero P&L return.

For buyers, the bargaining position to negotiate outcome-linked fees is genuine and growing. Parallel signals from large enterprise buyers in legal, finance, and technology services, where clients have begun refusing charges for AI-assisted work in vendor contracts, reinforce the trajectory. For providers, firms that do not rebuild compensation and pricing will be hollowed out from above by clients refusing to pay for what AI does, and from below by AI-native firms with senior-led delivery and outcome-based contracts. Tooling without economic rebuild buys time, not position.

How does AI turn trust into a measurable commercial term?

Trust is becoming a measurable commercial term. Failures from AI-generated work now translate into refunds, contract penalties, and lost mandates, not just reputational damage. The cost of an AI mistake has moved from a public relations matter to a profit-and-loss matter, and firms that demonstrate trust mechanisms credibly are gaining a commercial edge.

The Australian government's experience set the marker. A Deloitte report commissioned by the Department of Employment and Workplace Relations was found to contain fabricated court quotes and references to non-existent academic papers, traced to AI-generated content that had not been reviewed. Deloitte issued a partial refund of the AU$440,000 contract in early 2026. The case made the cost of an unverified AI deliverable concrete, public, and citeable in the next vendor evaluation.

Buyers had been signalling this requirement before the case made it material. The IBM Institute for Business Value's 2024 survey of 400 C-suite executives found that 90% want clear governance around AI in consulting services, 93% will only buy from organisations transparent about their AI use, and 82% are concerned about unethical AI use in consulting (IBM IBV, October 2024). A 2025 KPMG and University of Melbourne study across 47 countries reinforced the underlying problem: only 46% of users trust AI systems, and 66% use AI output without checking it.

Saudi Arabia's barring of PwC from new Public Investment Fund contracts in March 2025 added a parallel data sovereignty dimension. The decision was tied to data handling rather than AI, but the principle is the same: where trust is contractually defined and enforced, vendor consequences follow.

The structural consequence is that smaller and mid-tier firms with credible governance can compete against scaled firms whose AI deployments are partially opaque. Trust capability does not require Big 4 scale; it requires demonstrable controls, transparent methods, and accountability a procurement officer can verify. For buyers, AI output review clauses, transparency requirements, governance audit rights, and named accountability for AI-generated content are now standard in procurement templates. For providers, an explicit trust position is a commercial asset on dimensions where scale alone no longer wins.

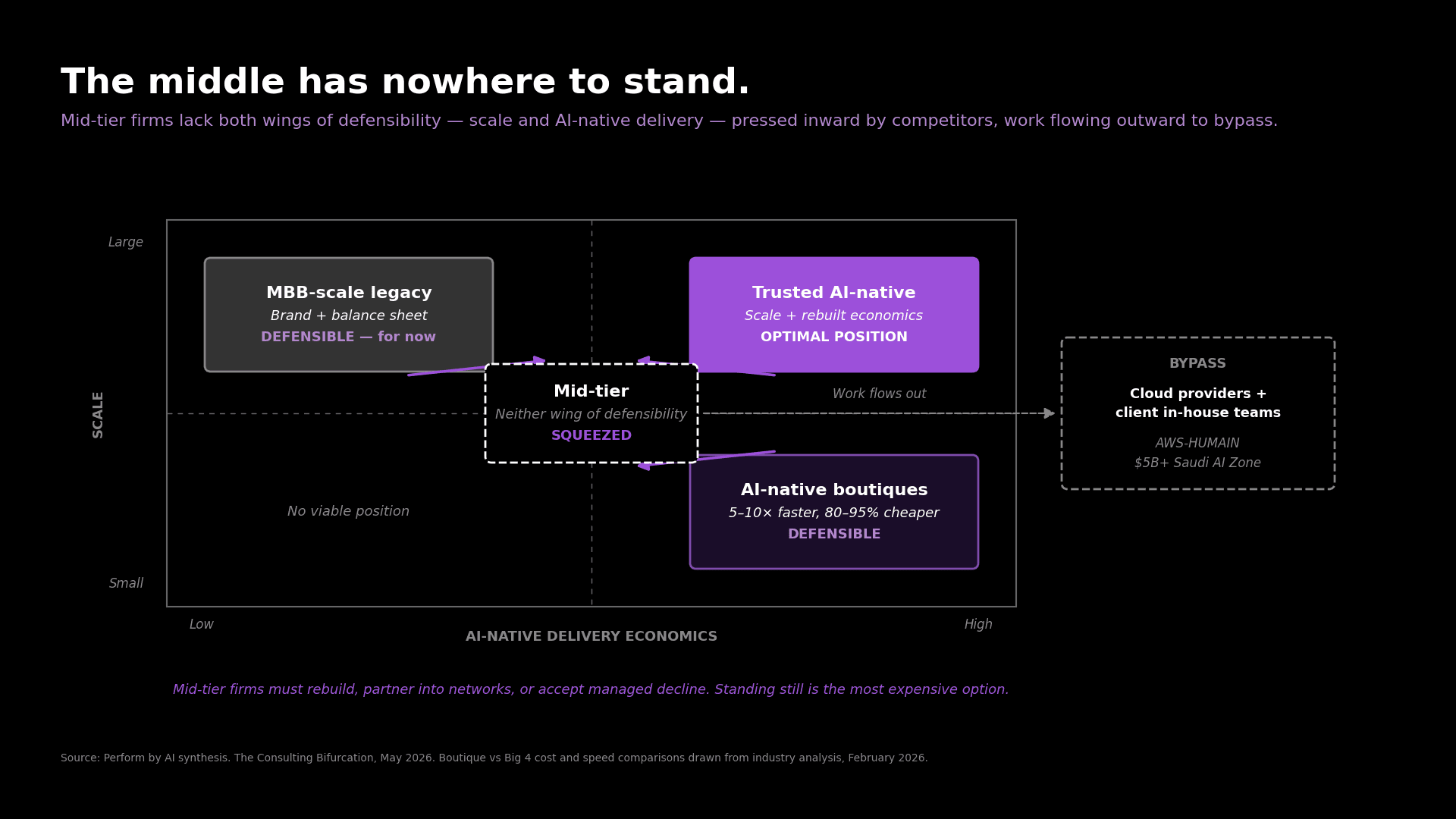

The middle is being squeezed from both sides

Mid-tier consultancies face pressure from below and above. AI-native boutiques deliver narrow problems faster and cheaper. Cloud providers and in-house teams take work that used to flow to external firms. The squeeze is structural, not cyclical, and firms in the middle without scale or specialisation are losing ground on both flanks at once.

Exhibit 2. Mid-tier consulting firms face structural pressure from AI-native boutiques below and hyperscaler advisory above; the squeeze is sharpest where neither scale nor specialisation defends the position.

From below, AI-native boutiques have changed what "fast" and "cheap" mean. Boutique AI engagements deliver narrow scopes on materially shorter timelines and at materially lower cost than Big 4 equivalents on comparable problems. The boutique model is senior-led; the Big 4 model is partner-sold and junior-delivered. Where the problem is narrow and AI-resolvable, the gap is too large to ignore.

From above, cloud providers are encroaching on advisory revenue. Microsoft, Google, and Amazon Web Services now bundle advisory with technology infrastructure, often at a price point traditional consultancies cannot match. The AWS-HUMAIN agreement of May 2025, a $5 billion-plus Saudi AI Zone combining cloud infrastructure with Saudi semiconductors, is the regional example.

In-house AI teams are the third pressure: large clients are building internal capability, often recruiting from consulting firms to do it, and the net effect is the loss of repeat work that fed the pyramid. The talent crisis sits underneath: AI now performs the entry-level analytical work that used to train junior consultants, the apprenticeship pipeline narrows, and senior-led delivery the next decade requires has fewer people training into it.

The strategic implication is that the mid-tier position is becoming the hardest to defend. Firms with MBB-scale brand and balance sheet have one set of options; firms with boutique-scale agility and AI-native delivery have another; mid-tier firms without either are exposed on both flanks. For buyers, tier-fit now matters more than name-fit; defaulting to scale is no longer a low-risk choice. For providers, mid-tier firms must rebuild, partner into networks that compete with both flanks, or accept managed decline. Standing still is the most expensive option.

Orchestration is becoming the practical answer to capability fragmentation

Buyers want one accountable partner, AI-augmented delivery, specialist breadth, and credible governance. No single tier of the consulting industry offers all four cleanly. The orchestration model fills the gap by combining accountability with networked specialist access, and is emerging as the practical answer to a capability fragmentation that AI has accelerated.

"the most in-demand consultants will be those who act as orchestrators and conduits"

IBM Institute for Business Value, October 2024

The fragmentation is real. The tech-services market has blurred between consultancies, hyperscalers, software vendors, and AI pure-plays (McKinsey, December 2025). Each holds part of what a complex programme requires. Big 4 firms carry breadth and brand but their AI delivery is uneven. AI-native specialists deliver narrow problems well but cannot anchor multi-track programmes. Hyperscalers bring capacity but advisory depth varies and conflict of interest sits closer to the surface than buyers prefer.

McKinsey's TMT analysis identifies six buyer factors: customisation, partnership ecosystem strength, consultative sales engine, domain expertise, line-of-business delivery, and outcome-based pricing. No single firm scores highly on all six. The selection problem has moved from "which firm" to "which combination of firms, under whose accountability."

The orchestrator does not deliver every component. The role is to define programme architecture, contract specialist capabilities, integrate the work, hold the governance line, and remain the accountable counterparty. The skill set sits closer to senior programme leadership than to partner-sold consulting. Peer-reviewed analysis reaches the same conclusion through different language: value creation, value proposition, and value capturing are being reshaped by the move from delivery to orchestration (HICSS, 2025).

The structural reason orchestration is emerging now is that AI has lowered the cost of accessing specialist capability. Networks of AI-fluent specialists, sector experts, and delivery teams that previously required Big 4 scale to coordinate at speed are now within reach of smaller and mid-tier firms with the right model.

For buyers, the new selection criterion is orchestration capability, not delivery capacity in isolation. For providers, orchestration creates a strategic option combining senior-led delivery with disciplined network access. It competes where pure global firms hit pricing constraints and pure boutiques hit breadth constraints, and is the structural answer to the trend 5 squeeze.

Why does the GCC consulting bifurcation look different from London or New York?

The GCC consulting bifurcation is structurally different from the global pattern because data sovereignty, localisation rules, and Year of AI compression operate as binding constraints on market entry and delivery. The result is a market that favours firms combining global capability with local depth, AI fluency, and governance discipline simultaneously.

The market is large and the timeline is compressed. The GCC management consulting market reached $7.15 billion in 2026 (Mordor Intelligence, January 2026). Saudi Arabia accounts for 45% of regional spend; the Vision 2030 pipeline exceeds $500 billion. The UAE Digital Strategy commits AED 13 billion to over 200 AI solutions across government. Saudi designated 2026 the Year of AI in March 2026 under Crown Prince patronage. Infrastructure is at scale: Hexagon, the world's largest government data centre at 480 megawatts, is operational, and AWS-HUMAIN's $5 billion Saudi AI Zone was announced in May 2025. The buyer is government-led with fixed timelines.

Localisation rules are binding, not negotiable. Saudi Arabia barred PwC from new Public Investment Fund work in March 2025 over data handling concerns, the public marker that compliance is enforced. The Saudi Regional Headquarters programme requires at least 15 local staff to qualify for government contracts. The Saudi Personal Data Protection Law governs how deliverables are processed and stored. In delivery work across the region, these conditions shape selection and execution from the first procurement conversation.

Neither pole of the global bifurcation fits cleanly. Pure global Big 4 firms carry scale but face data residency constraints, RHQ thresholds, and local-staff requirements. Pure AI-native boutiques carry agility but lack governance breadth, regulatory standing, and local presence. Large GCC public-sector institutions, including organisations served by Big 4 firms today, increasingly want a partner combining global capability with local rootedness, AI fluency, and accountability. The orchestrator profile from the wider market structure fits this regional pressure closely.

For buyers, selection now requires local depth, AI fluency, governance breadth, and orchestration capability simultaneously. For providers, regional firms with the right model hold a strategic 18- to 36-month window. For investors and new entrants, entry strategy is regulatory before commercial: pure global expansion hits RHQ and PDPL friction, pure AI-native expansion hits governance and breadth gaps, and the orchestrator profile is the more defensible path.

Looking ahead

The next 18 to 36 months will determine which firms occupy each side of the bifurcation. AI use will continue to converge across the industry; demonstrating it will not by itself distinguish a serious firm from a positioning one. The harder threshold is the second breakpoint: rebuilt economics. Firms that have actually changed how they price, how they staff, how they govern AI output, and how they hold accountability will read very differently from firms that have layered AI onto an unchanged model.

For buyers, selection criteria will tighten through 2027 as AI procurement becomes more disciplined. The firms that win mandates will be those that can show outcome-linked pricing, transparent AI methods, named accountability, and measurable governance, not the firms that rely on brand alone. For providers, the strategic options narrow with each quarter. MBB scale and balance sheet defend one position; AI-native depth defends another; orchestration capability defends a third. Mid-tier firms without a clear position face structural pressure that capital alone cannot reverse.

In the GCC, the structural variant is set. The 18- to 36-month window for building local-rooted, AI-fluent, governance-credible orchestration capability is open and compressing. Investors and new entrants reading the market correctly will recognise that pure global expansion and pure boutique entry both encounter constraints the orchestrator profile does not.

By 2028, the firms still measured by AI revenue alone will have lost the more important conversation about how they make it.