In our 2026 work with Gulf leaders, ranging from family-run mid-market firms to large enterprises, the same three demands now land in the same quarterly review: cut costs, demonstrate AI ROI, accelerate growth. The cost pressure behind those demands is not transient. The two default responses, cutting deeper or investing in more AI, both fail empirically in 2026. The answer is neither alone; it is a four-lever model that pairs productivity, strategic reallocation, selective AI, and reach expansion.

A permanently higher cost floor demands a system response, not a single lever. The four-lever model pairs productivity, strategic reallocation, selective AI, and reach expansion to move cost base, capital base, and revenue base together. The cash-positioned business runs all four in parallel; the cash-constrained business sequences from productivity, letting savings fund the rest. A 90-day plan, sequenced by cash position, brings the model inside a quarter.

This analysis draws on multilateral institutional research, industry CEO surveys, market data, public firm disclosures, and regional analyst commentary from late 2025 through May 2026. Sources include the International Labour Organization's Arab States employment scenarios (May 2026), EY's 2026 CEO Priorities survey (n=1,200) and 2026 CEO Outlook, the S&P Global UAE PMI release (March 2026), Atlantic Council regional analysis, Middle East Institute commentary, and 2026 enterprise research from Accenture (n=3,650), BCG, McKinsey, PwC (n=1,217), and the World Economic Forum, supported by OECD analysis of generative AI productivity effects.

The cost shock is already the new baseline

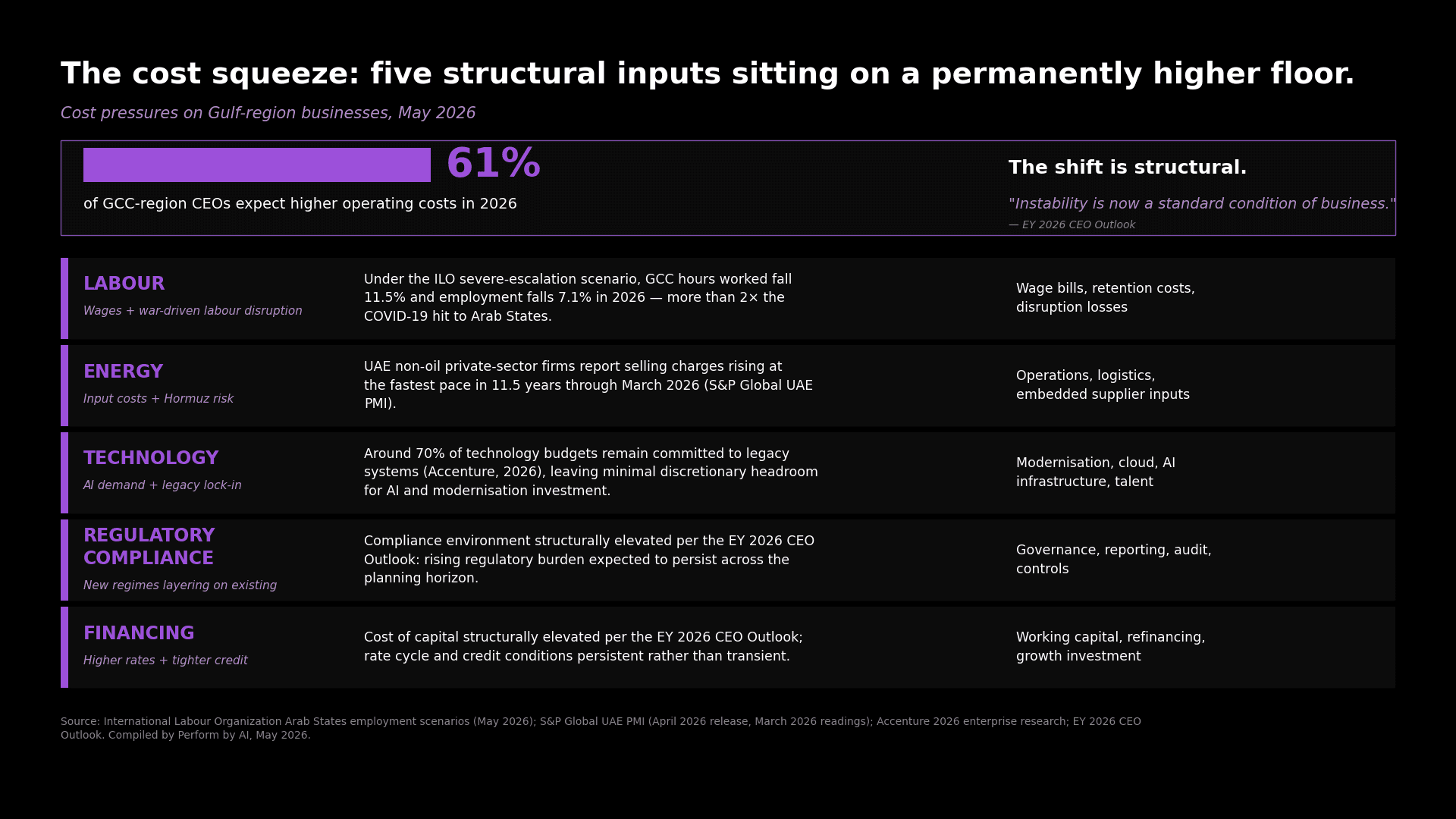

The cost pressure on Gulf region businesses is not a spike that will pass; it is the new baseline the decade ahead will run on. UAE non-oil private-sector firms reported selling charges rising at the fastest pace in 11.5 years through March 2026, with business confidence falling to a five-year low amid Strait of Hormuz disruption (S&P Global UAE PMI, April 2026). The labour-market scenarios are heavier still: under the International Labour Organization's severe-escalation scenario, GCC hours worked fall 11.5% and employment falls 7.1% in 2026, more than twice the COVID-19 hit to Arab States in 2020 (ILO, May 2026).

The pressure layers onto a structural backdrop that pre-dates the war: GCC GDP per capita has plateaued for decades as population growth outpaced output growth, with Vision 2030 designed as the policy response to that plateau, not to today's conflict (Atlantic Council, May 2026). The framing CEOs themselves use is unsentimental: 'instability is now a standard condition of business' (EY, May 2026).

If this is the new baseline, the default responses Gulf region business leaders reach for first do not survive contact with it.

"The impact of the conflict will not stop at energy price hikes. It will spread to various sectors and last years."

— Umair Waqas, Al Jazeera, 21 May 2026

Exhibit 1. Five structural input pressures form the new cost baseline for Gulf-region businesses; 61% of CEOs expect higher operating costs in 2026 against 16% expecting reductions.

Why the two default responses now fail

Both default responses fail empirically, and they fail for different reasons that resolve to the same underlying constraint.

Cost-cutting alone fights structural gravity. EY's 2026 CEO Outlook finds 61% of CEOs expecting higher operating costs in 2026 against only 16% expecting reductions, and frames the shift as structural in nature: labour, energy, technology, regulatory compliance, and financing inputs are all elevated and likely to persist. A second pressure compounds the first: roughly 70% of technology budgets still support legacy systems (Accenture, 2026), which means most discretionary spend sits in commitments that cuts alone cannot easily redirect. The lever pulled in isolation faces a permanently higher cost floor on one side and a budget that cannot redeploy itself on the other.

AI investment alone fares no better. BCG's 2026 AI-first cost-advantage research finds that roughly 60% of companies report minimal or no value from AI investment despite significant effort, and that the firms capturing value follow a 10-20-70 rule: 10% of value comes from algorithms, 20% from technology and data, 70% from process and workflow redesign. McKinsey's 2026 measurement research finds 60% of organisations have not yet seen enterprise-wide EBIT impact from their AI programmes, with the gap between AI activity and AI impact widening.

BCG's parallel productivity research is sharper on the mechanism: AI lets organisations produce more and respond faster, but in most cases that capacity is not strategically redeployed, and cost bases stay unchanged or even rise as new technology layers on. Survey evidence converges: Accenture's 3,650-executive Pulse of Change finds 86% increasing AI investment in 2026 but only 21% redesigning end-to-end processes with AI at the core, while PwC's 1,217-executive AI fitness study finds 20% of organisations capturing 74% of AI-driven returns.

Both defaults fail for the same reason: a permanently higher cost floor demands a system response, not a single lever. Cutting compresses the cost base without expanding the revenue base; investing in AI expands capacity without redirecting how the business works. The four-lever model is built to break this trap.

What three levers must pair with AI?

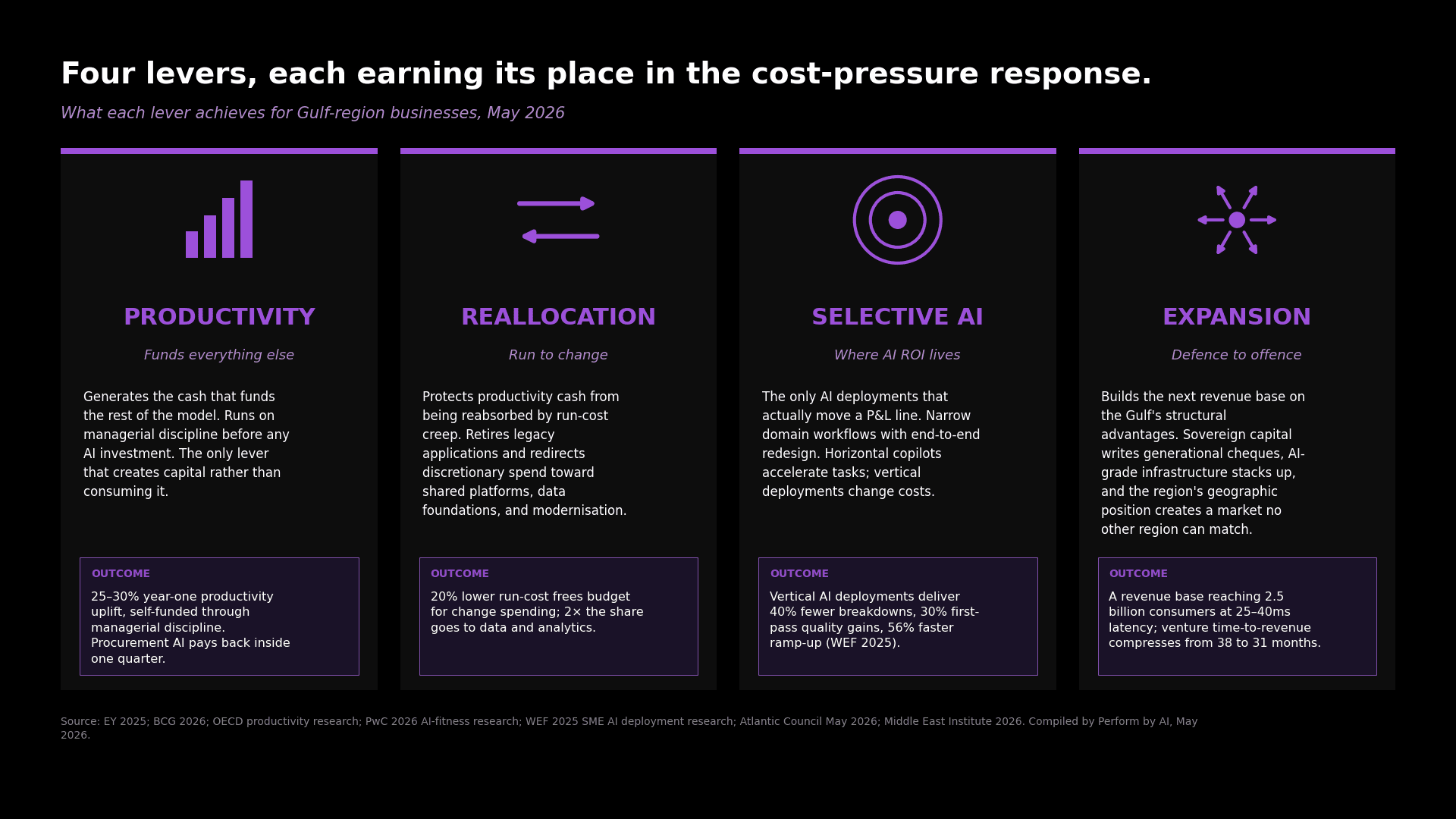

What three levers must pair with AI? Productivity, strategic reallocation, and reach expansion. Together with selective AI they form a four-lever model that moves cost base, capital base, and revenue base together: the system response a permanently higher cost floor demands. The cash position decides the order, not the size of the business.

"These leaders recognize that their AI and cost reduction agendas are inseparable."

— BCG, How Leaders Build an AI-First Cost Advantage, 2026

Exhibit 2. The four-lever response: productivity funds the model, reallocation protects the gains, selective AI delivers ROI, expansion builds the next revenue base.

Productivity first: the lever that funds everything else

Productivity is the lever that funds the rest, and it requires no AI to start.

Most recoverable productivity in services-heavy businesses sits in the hidden factory of employee ineffectiveness: time lost to mailbox triage, agenda noise, document management, and meeting overhead. EY's 2025 services-productivity research finds most organisations operate at 50–60% effective utilisation on value-add activities, with up to 20% productivity available to a leader who attacks the hidden factory alone, without significant technology spend. Layered on top, operating-model and FTE-allocation discipline typically extracts a further 10–20%; integrated production and capacity planning, 10–15%; and a tight performance-management cadence around the PDCA cycle, the strongest single lever at 25–50%.

Where AI does fit at this stage of the lever, it pays back inside one quarter. BCG's 2026 cost-advantage research on procurement AI reports 5–25% supplier-review savings in 3–6 months, 5–10% specification-review savings in the same window, and 5–15% inventory-optimisation savings in 3–9 months. Procurement is the canonical first-AI deployment because the data and the workflows are tractable, and the savings cycle is short enough to land before the next quarterly review.

The mechanic transfers to smaller and mid-market operators. Evaluated cohort programmes built on lean-management training and peer networks have lifted productivity 50%+ across thousands of firms, at per-firm costs in the low hundreds of US dollars (OECD productivity-programme research, 2019). The design principles are consistent: simple rules accessible to non-specialists, low per-firm costs to scale reach, and intermediary organisations for delivery instead of parallel programme structures. At unit-of-work level, the WEF's 2025 SME manufacturing AI research confirms the same mechanic transfers cleanly: predictive maintenance, defect detection, and workforce-optimisation systems all deliver material gains at intervention budgets a Gulf mid-market or family-business operator can absorb.

For cash-constrained businesses, this lever is the starting point and the funding source for the rest. A realistic 25–30% year-one productivity gain, drawn from managerial discipline before technology spend, generates the cash to fund strategic reallocation, selective AI, and reach expansion across years one to three. For cash-positioned businesses, the lever runs in parallel; productivity capacity freed at the top compounds into the reallocation and AI that follow.

Strategic reallocation: moving money from run to change

Productivity cash without reallocation discipline gets absorbed back into the run base. Most companies under cost pressure spend more on AI; the few that pull margin out of AI spend differently.

PwC's 2026 AI-fitness research finds AI leaders are 1.3× as likely as the rest to reallocate financial and human resources toward high-value AI projects as priorities shift, and 2× more likely to eliminate outdated and costly applications, systems, and infrastructure to fund the new ones. Reallocation is a discipline, not a budget line.

The pattern shows up in IT-spending archetypes. The companies pulling AI value run lean on infrastructure, around 20% lower run-cost than peers, direct most application spending toward modernisation and new capabilities, invest twice as much in data and analytics, and put 1.5 to 4 times more of their tech budget into internal staff working on change. Companies adding AI investment on top of an existing run-heavy IT base find the new spend crowds out other value-creating projects, change capacity caps out, and the AI programmes themselves slow. Survey data from 17 global companies through late 2025 shows AI consuming up to a third of change budgets while adding to run costs.

The discipline has three operating moves: retire what no longer earns its place in the run base; point change spending at shared platforms and data foundations, not vertical pilots; use AI to remove work and systems, not layer onto them. None requires net new capital.

For cash-constrained businesses, the reallocation lever activates as the productivity lever's cash arrives in months six to nine, protecting that cash from being absorbed by run-cost creep and abandoned pilots. For cash-positioned businesses, reallocation runs alongside productivity from quarter one, freeing change capacity for selective AI and reach expansion to follow.

Selective AI: where the ROI actually lives in 2026

The ROI lives in narrow vertical deployments with end-to-end workflow redesign and measurement discipline; it does not live in broad horizontal pilots layered onto existing operations.

The deployments that pay back are domain-specific and outcome-bounded. At unit-of-work level, manufacturing AI deployments at SME scale in 2025 produce 40% reductions in unplanned breakdowns from predictive maintenance, 30% gains in first-pass quality from defect detection, and 56% reductions in production ramp-up time from workforce-optimisation systems (WEF, 2025). At enterprise scale, the Gulf-region case is sharper. ADNOC's AiPSO platform, launched with SLB in November 2025, has engineers diagnosing and optimising wells in minutes, not days, with reservoir-engineering tasks running 10× faster; deployment is scaling from 8 fields to 25 by 2027 (ADNOC, November 2025). These are not horizontal copilots; they are vertical workflows engineered into the operating model.

The pattern that does not pay back is also concrete. Horizontal AI tools, the chatbots, summarisers, and copilots, improve employee experience and accelerate individual tasks but rarely change a P&L line. The leaders in the 2026 measurement research are not deploying more horizontal tools; they are automating end-to-end workflows in specific domains such as claims processing, customer service, and demand planning, and they measure against financial outcomes, not activity volume.

The discipline that separates the two patterns is measurable. McKinsey's 2026 measurement research lays out a five-layer cascade leaders use to define and track AI value: financial impact at the top, then strategic outcomes, operational KPIs, user adoption, and technical performance at the base, all tied through stage gates from pilot to MVP to initial scaling to full scale. Accenture frames the maturity progression in three phases: Siloed AI delivers efficiency and productivity inside two to three years; Structural AI delivers growth and new business models; Systemic AI compounds into market leadership.

For cash-constrained businesses, the lever starts in Phase 1 Siloed: pick one or two domain workflows where the data and value chain are tractable, deploy with the five-layer measurement cascade in place from day one, and scale only what proves out at the financial-impact layer. For cash-positioned businesses, the lever runs multiple Phase 1 deployments in parallel and ladders into Phase 2 inside 18 to 36 months as foundations harden.

Reach expansion turns defence into offence

Reach expansion turns defence into offence. The first three levers protect margin; the fourth one builds the next revenue base.

The structural conditions for the Gulf-region operator on this lever are exceptional. Sovereign capital writes generational-horizon cheques no other class of investor can match; energy is cheap and abundant, now increasingly under the same roof as compute; and the geography places the region within 25–40ms round-trip latency of 2.5 billion data consumers from Mumbai to Cairo, against 150–200ms from the US east coast. These conditions are why eight to ten gigawatts of AI compute capacity are being built across the GCC by 2030, and why the Emirati ambassador to Washington framed the regional posture in May 2026 not as hedging but as doubling down (Middle East Institute, 2026).

At firm level, AI does to reach what cost transformation does to margin: it removes friction the operator could not previously cross. AI leaders globally are 2.6 times as likely as the rest to use AI to reinvent their business model and 1.8 times as likely to spot emerging value pools that sit between industries. The five operational concentration points are consistent across the 2026 research: real-time individualised customer experience; resilient end-to-end operations; accelerated research and development; predictive strategic planning; and personalised talent systems (WEF, 2026).

The 2025 new-business-building research anchors the velocity case: roughly 60% of corporate ventures generated over US$10M in revenue (up from 45% in 2023); time-to-revenue fell from 38 months to 31 months; teams with AI-augmented build report acceleration up to 5×. The point for a Gulf-region leader is that the venture economics now favour speed over scale, and the region's combination of sovereign capital and AI-grade infrastructure makes the speed-over-scale play more available here than in most markets.

For the Gulf-region operator, reach expansion is not a future scenario. The sovereign capital is committed, the AI infrastructure is being built now, and the 25–40ms latency to 2.5 billion data consumers is geographic, not transitional. The firms acting on this lever first will set the terms of regional growth through 2030; the firms waiting will compete for share in a market built around someone else's positioning.

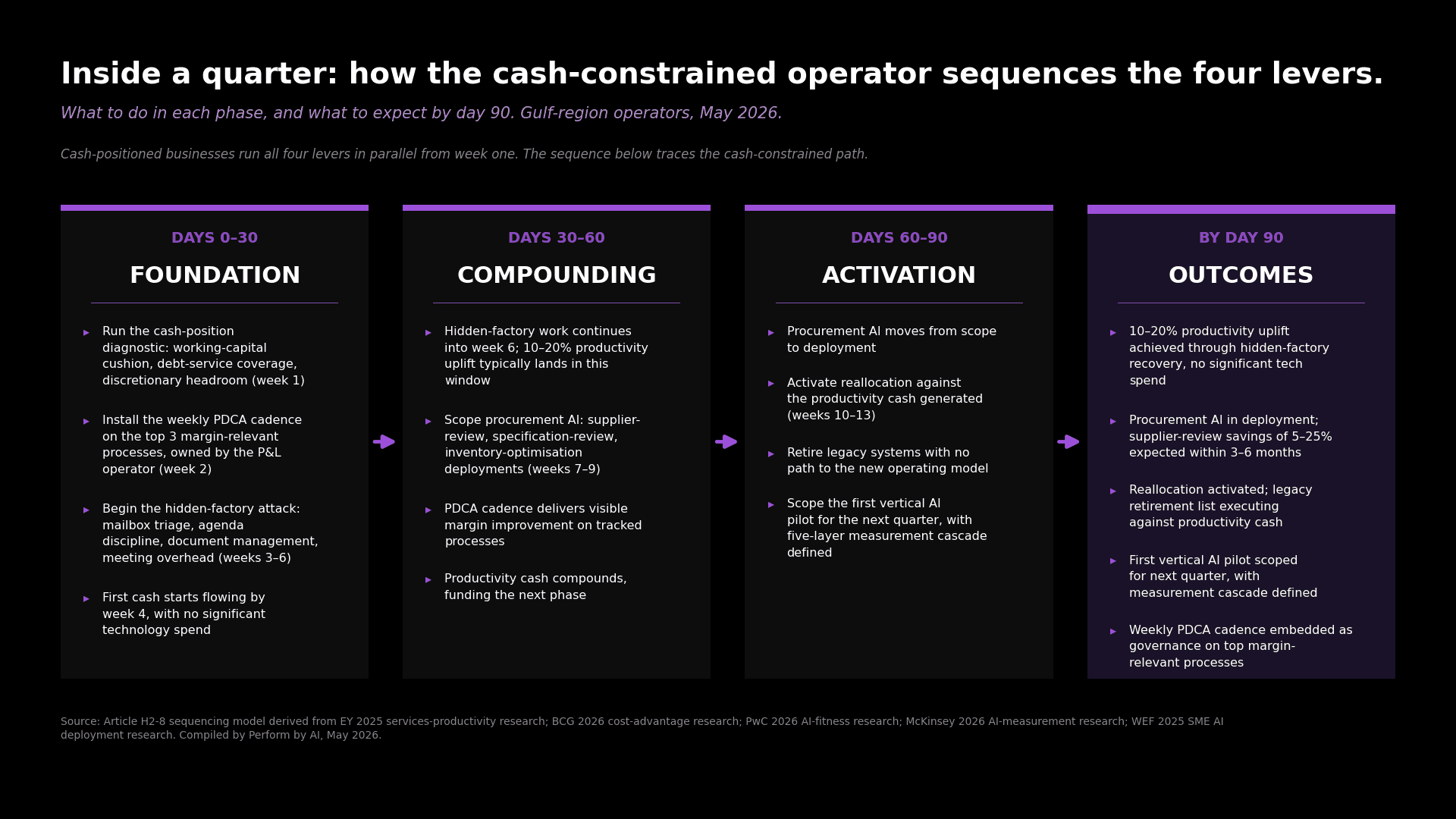

What does a 90-day plan look like under cost pressure?

A 90-day plan under cost pressure starts inside a quarter, not across a decade. Cash-positioned businesses run all four levers in parallel from week one. Cash-constrained businesses sequence from productivity, letting weeks three to nine fund reallocation by weeks ten to thirteen and scope the first vertical AI pilot for the next quarter.

The cash-position diagnostic is week one regardless of starting position. Three readings place the business in one of two categories: working-capital cushion in weeks of operating cost, debt-service coverage against committed cash flows, and discretionary headroom against fixed-cost baseline. The cash-positioned business reads comfortable on all three; the cash-constrained business reads tight on one or more, which rules out parallel investment across four levers. By week two, a weekly PDCA performance cadence covers the top three margin-relevant processes, run by the operator who owns the P&L.

For cash-constrained businesses, weeks three to six attack the hidden factory: mailbox triage, agenda discipline, document management, meeting overhead. A 10 to 20% uplift typically lands inside this window with no significant technology spend. The cash starts in week four. Weeks seven to nine scope procurement AI; supplier-review deployments commonly land 5 to 25% savings inside three to six months. Weeks ten to thirteen activate reallocation against the cash these gains generate, and scope one vertical AI pilot for the next quarter.

For cash-positioned businesses, all four levers run in parallel. Productivity work attacks the hidden factory alongside integrated production and capacity planning; the PDCA cadence covers the top six margin-relevant processes from day one. Reallocation begins with an audit of the run-cost base and a retirement list of legacy systems with no path to the new operating model. Two vertical AI pilots scope in parallel, with the five-layer measurement cascade installed before deployment. Reach-expansion scenario work begins by week six against a sovereign-capital or regional-partner thesis.

Exhibit 3. The 90-day plan for cash-constrained Gulf-region businesses sequences the four levers from foundation through compounding and activation to measurable outcomes by day ninety.

The Gulf-region business leader sits at the most concentrated intersection of cost pressure, AI build-out, and growth optionality the regional economy has seen. Vision 2030 was the structural answer to how the region grows when oil revenue is spread across a growing population. The 2026 conditions are the test of that answer. Cutting costs alone will not pass the test. Investing in AI alone will not pass it either. Pairing productivity, strategic reallocation, selective AI, and reach expansion, sequenced by cash position and calibrated to the business, is the operating posture this baseline rewards. Gulf-region business leaders building toward 2028 will be measured not by AI spend, but by margin protected, capital redirected, work redesigned, and reach extended.